Buying a salvage or rebuilt title car can save you thousands, but getting insurance can be tricky. This guide breaks down everything budget buyers need to know—from understanding salvage and rebuilt titles to choosing the right coverage. Learn how to navigate inspections, repair documentation, and insurer requirements so you can protect your investment and drive legally without overspending.

What Is a Salvage Title Car?

A salvage title car is a vehicle that has been declared a total loss by an insurance company. This usually happens when the cost to repair the car is higher than a certain percentage of its value. In simple terms, the insurer decides it’s not worth fixing — at least from their financial point of view.

For budget buyers, this is where opportunity starts. These cars often end up at online auctions for a much lower price. You might see a 3–5-year-old car selling for half of its market value just because it has a salvage title.

But there’s a catch. A salvage title means the car has a history of serious damage. It could be repairable, but it also comes with risks — including problems with insurance, which is exactly what many buyers only discover after purchase.

When Does a Vehicle Receive a Salvage Title

A vehicle gets a salvage title when an insurance company determines it is a “total loss.” This doesn’t always mean the car is completely destroyed. It simply means repairing it is not financially reasonable for the insurer.

For example, imagine you buy a used car worth $10,000. After an accident, the repair estimate comes in at $7,500. Many insurance companies have a threshold (often around 70–80% of the car’s value). Once repairs cross that line, they write the car off and issue a salvage title.

This is why you’ll often find cars at auctions that don’t look “that bad” but still carry a salvage title. From a buyer’s perspective, they might seem like a great deal — and sometimes they are — but the title status will follow the car forever.

Common Reasons Cars Become Salvage

Not all salvage cars are the same. Some have minor cosmetic damage, while others have serious structural issues. Understanding why a car received a salvage title helps you decide whether it’s worth the risk.

Major Accident Damage

This is the most common reason. The car has been involved in a crash that caused significant damage — often to the frame, engine components, or safety systems.

For example, a front-end collision might damage the bumper, hood, radiator, airbags, and sensors all at once. Even if the car can be repaired, the total cost quickly adds up. That’s when insurance companies step in and declare it a total loss.

For buyers, this type of damage can be fixable, but it requires careful inspection. Poor repairs can lead to long-term safety issues.

Flood or Water Damage

Flood-damaged cars are some of the riskiest salvage vehicles. Water can get into the engine, transmission, wiring, and electronics.

A car might look clean on the outside, but inside it could have corrosion, mold, or failing electrical systems. Problems may not show up immediately. You might drive it for a few weeks and then suddenly deal with electrical failures.

Many experienced buyers avoid flood cars completely, even if the price looks tempting.

Theft Recovery

Sometimes a car is stolen and not recovered for a long time. The insurance company pays the owner and writes the car off. If the vehicle is later found, it may receive a salvage title.

In many cases, theft recovery cars have little or no physical damage. Maybe the interior is worn or parts are missing, but structurally the car can be in good shape.

This is one of the few situations where a salvage car can be a very good deal — especially for buyers looking to save money with minimal repair work.

Fire or Natural Disaster Damage

Cars can also receive salvage titles after fires or natural disasters like hailstorms, hurricanes, or earthquakes.

Fire damage is especially serious because it can weaken metal parts and destroy wiring. Even small fires can lead to expensive hidden issues.

Natural disasters vary. Hail damage might only affect the body panels, making it one of the easier types to repair. On the other hand, cars damaged by hurricanes often combine water and impact damage, which increases the risk.

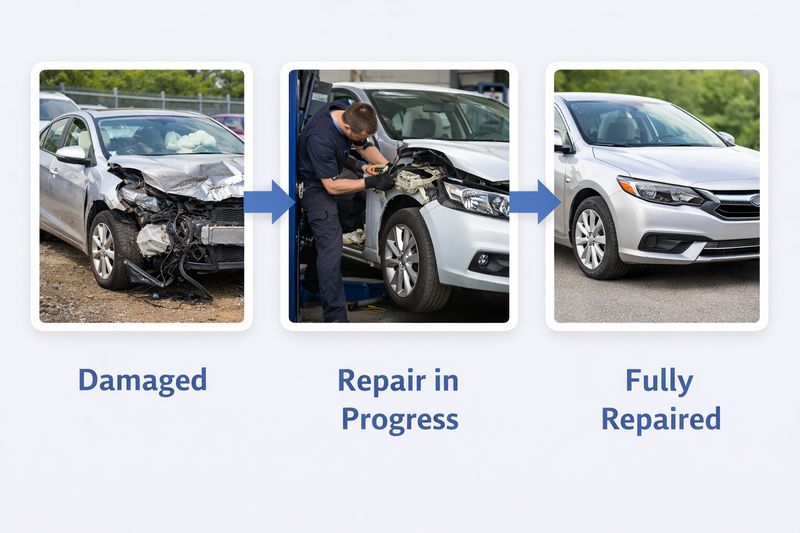

What Is a Rebuilt Title?

A rebuilt title is given to a car that once had a salvage title but has been repaired and approved for road use again. In simple terms, the car was previously considered a total loss, but someone fixed it, passed inspections, and made it legal to drive.

For budget buyers, this is often the sweet spot. You’re not dealing with a completely damaged vehicle anymore, but you’re still getting a lower price compared to a clean title car. For example, a rebuilt car might cost 20–40% less than a similar vehicle with no damage history.

However, the key thing to understand is that the history doesn’t disappear. Even after repairs, the rebuilt title stays on record permanently. That means future buyers, insurers, and even lenders will always see that the car was once salvage.

Difference Between Salvage Title and Rebuilt Title

The main difference comes down to usability and condition.

A salvage title means the car is not road legal. You can’t legally drive it on public roads until it has been repaired and inspected. At this stage, it’s essentially a project car.

A rebuilt title, on the other hand, means the car has already gone through repairs and passed a state inspection. It is now considered safe enough to be driven again.

Think of it this way:

- Salvage = damaged and not approved for the road

- Rebuilt = repaired and approved for the road

For example, many buyers purchase salvage cars from online auctions, fix them, and then apply for a rebuilt title. Others prefer to skip the repair process and buy a car that’s already rebuilt, even if it costs more.

Compare Salvage and Rebuilt Cars Before You Bid

Once you understand the difference between salvage and rebuilt title cars, the next step is comparing real auction listings. Review title status, damage type, mileage, and prior sale history to identify vehicles that offer the best value with a risk level that matches your budget.

- ✅ Filter inventory by salvage or rebuilt title

- ✅ Review damage type before bidding

- ✅ Access past auction history and photos

- ✅ Compare pricing across similar vehicles

When a Salvage Car Becomes Road Legal Again

A salvage car becomes road legal only after it goes through a specific process. This process can vary slightly depending on the state, but the general steps are similar.

First, the car must be fully repaired. This includes fixing both visible and hidden damage — not just making the car look good, but making it safe.

Next comes a state inspection. This is not a basic safety check. Inspectors often look closely at the vehicle to confirm that repairs were done properly and that no stolen parts were used.

You’ll usually need to provide documentation, such as:

- receipts for parts

- proof of repairs

- photos showing the damage before and after

Once the car passes inspection, the state issues a rebuilt title. Only after that can you legally register, insure, and drive the vehicle.

This is why many budget buyers choose to buy already rebuilt cars. It saves time, avoids paperwork, and reduces the risk of failing inspection.

Why Rebuilt Titles Still Affect Insurance

Even though a rebuilt car is road legal, insurance companies still treat it differently from a clean title vehicle. The reason is simple: risk.

Insurers know the car was previously declared a total loss. That raises several concerns. There could be hidden damage that wasn’t properly repaired. The structural integrity might not be the same as before. And in case of another accident, it’s harder to determine the true value of the car.

For example, if you get into an accident with a rebuilt car, the insurance payout will usually be lower than for a clean title vehicle. That’s because the car’s market value is already reduced.

Some insurance companies may also limit coverage options. You might easily get liability insurance, but full coverage (including collision and comprehensive) can be harder to obtain or more expensive.

This is something many first-time buyers don’t expect. They save money buying the car, but later realize insurance is more limited than they thought.

Can You Insure a Car With a Salvage Title?

In most cases, you cannot insure a car with a salvage title — at least not in the way most drivers expect. A salvage title usually means the car is not road legal, so insurance companies see no reason to offer standard coverage.

For many budget buyers, this becomes a problem after purchase. You find a cheap car at auction, win the bid, and then realize you can’t legally drive it — and you also can’t insure it for regular use yet.

That said, there are a few exceptions. But overall, if your goal is to drive the car on public roads, you’ll almost always need to convert the salvage title into a rebuilt title first.

Why Most Insurance Companies Refuse Salvage Titles

Insurance companies avoid salvage title cars because they represent a high level of uncertainty.

First, the condition of the vehicle is unclear. A salvage car may have serious structural damage, missing safety systems, or hidden issues that are not visible during a basic inspection. From an insurer’s point of view, this increases the risk of accidents and future claims.

Second, the car is not legally roadworthy in most states. If the vehicle isn’t approved for driving, insurers cannot offer standard policies like liability or full coverage.

Third, it’s difficult to determine the car’s value. After major damage, there is no clear market price. This creates problems when calculating premiums or potential payouts.

For example, imagine trying to insure a car that was heavily damaged in a crash but hasn’t been repaired yet. The insurer has no reliable way to assess how safe it is or how much it’s worth. In most cases, they simply refuse coverage.

Situations When Salvage Cars May Be Insured

While full insurance is rarely available, there are limited situations where a salvage car can be insured.

One example is storage or transport insurance. If the car is not being driven but needs to be protected while parked, stored, or shipped, some insurers may offer basic coverage. This protects against risks like theft, fire, or damage during transportation.

Another case is project or restoration coverage. Some specialty insurers may offer policies for cars that are being repaired, especially if the owner can show a clear restoration plan.

However, these policies are very limited. They do not allow you to legally drive the car on public roads. They are designed to protect the asset, not to replace standard auto insurance.

For a typical buyer who wants to fix and drive the car, these options are only temporary solutions.

Why Insurance Usually Requires a Rebuilt Title First

Insurance companies almost always require a rebuilt title before offering standard coverage. This is because a rebuilt title confirms that the car has been repaired and passed an official inspection.

From the insurer’s perspective, this reduces uncertainty. The vehicle is now considered roadworthy, and there is documentation showing what was repaired and how.

For example, once a car passes a state inspection and receives a rebuilt title, you can usually apply for liability insurance. This is the minimum required to drive legally in most places.

Without that rebuilt status, insurers have too many unknowns. They don’t know if the brakes, airbags, or frame are safe. They also don’t know if the repairs meet any standards at all.

This is why experienced buyers plan ahead. They don’t just look at the purchase price of a salvage car — they think about the full process: repairs, inspection, title conversion, and only then insurance.

Can You Insure a Car With a Rebuilt Title?

Yes, you can insure a car with a rebuilt title. In fact, this is the point where insurance becomes realistic for most budget buyers. Once a vehicle has been repaired, inspected, and officially declared roadworthy, insurance companies are more willing to work with it.

However, “can be insured” does not always mean “insured the same way as a clean title car.” You may face some limitations. Coverage options can be narrower, and payouts are usually lower. Still, compared to a salvage title, a rebuilt title gives you access to standard insurance policies — which is what you need to legally drive.

For many buyers, this is the step where the car finally becomes usable in everyday life.

Why Rebuilt Cars Are Easier to Insure

Rebuilt cars are easier to insure because they have already gone through a formal repair and inspection process. This gives insurance companies more confidence in the vehicle’s condition.

Instead of guessing how damaged the car might be, insurers can rely on:

- inspection results

- repair documentation

- photos and receipts

This reduces uncertainty. The car is no longer a “question mark” like a salvage vehicle.

For example, if you buy a rebuilt car that passed inspection and has clear records of replaced parts, an insurer can evaluate it more accurately. They still see it as higher risk compared to a clean title car, but it’s a manageable risk — not an unknown one.

That’s why many budget buyers prefer buying already rebuilt cars instead of dealing with salvage vehicles from scratch.

Minimum Insurance Requirements to Drive Legally

To drive legally, you typically need at least liability insurance. This is the most basic type of coverage and is required in almost every state.

Liability insurance covers damage you cause to other people and their property. It does not cover your own car.

For example, if you rear-end another vehicle, liability insurance pays for the other driver’s repairs and medical costs. But your rebuilt car will not be covered unless you have additional insurance.

This is important for budget buyers. Many people choose rebuilt cars to save money, and they often stick with liability-only coverage to keep insurance costs low.

However, this comes with a trade-off. If your car is damaged in an accident, you’ll have to pay for repairs out of pocket.

State Laws That Affect Insurance Options

Insurance rules for rebuilt title cars can vary depending on the state where the vehicle is registered.

Some states are more flexible and allow a wider range of coverage options. Others are stricter and may limit what insurers can offer for rebuilt vehicles.

State laws can affect:

- how inspections are conducted

- what documents are required

- whether full coverage is available

- minimum liability limits

For example, one state may allow you to easily get both liability and comprehensive coverage for a rebuilt car, while another may make it harder or require additional inspections.

If you’re buying a car from a U.S. auction and planning to export or register it in a specific state, it’s important to check local requirements in advance.

A common mistake is buying a cheap rebuilt car without researching insurance rules. Later, the buyer discovers limited coverage options or higher-than-expected costs.

What Types of Insurance Are Available for Rebuilt Title Cars?

Once a car has a rebuilt title, you can usually access several types of insurance coverage. However, not every insurer will offer the full range, and some policies may come with limitations.

For budget buyers, the key is understanding what each type of insurance actually covers — and whether it’s worth paying extra for it. In many cases, people choose a cheaper rebuilt car and then try to balance protection with affordable premiums.

Here are the main types of insurance you can expect.

Liability Insurance

Liability insurance is the most basic and most important type of coverage. In most states, it’s legally required if you want to drive your car on public roads.

This insurance covers damage you cause to other people — not your own vehicle. It usually includes:

- property damage (repairs to another car or property)

- bodily injury (medical costs for other drivers or passengers)

For example, if you accidentally hit another car, liability insurance will pay for their repairs. But if your rebuilt car is damaged, you’ll have to cover those costs yourself.

Most budget buyers start with liability-only coverage because it’s the cheapest option. It allows you to drive legally without adding high monthly insurance costs.

Collision Coverage

Collision coverage pays for damage to your own car after an accident, regardless of who is at fault.

This can be useful if you rely on your vehicle daily and can’t afford unexpected repair costs. For example, if you slide on a wet road and hit a barrier, collision coverage will help pay for fixing your car.

However, with rebuilt title cars, this type of coverage is not always easy to get. Some insurers may refuse it, while others may offer it at a higher price.

Another important point is the payout. Because rebuilt cars have lower market value, the insurance company will pay less compared to a clean title car. Sometimes the payout may not fully cover repair costs, especially if the car was already inexpensive.

Comprehensive Coverage

Comprehensive coverage protects your car from non-accident-related risks. This includes things like:

For example, if your rebuilt car is stolen or damaged by a falling tree, comprehensive coverage can help cover the loss.

For budget buyers, this type of insurance can make sense if the car still has decent value or if you live in an area with higher risks (like frequent storms or theft).

Like collision coverage, comprehensive insurance may be limited or more expensive for rebuilt cars. Insurers are cautious because the vehicle already has a damage history.

Uninsured and Underinsured Motorist Coverage

This type of insurance protects you if you’re involved in an accident with a driver who has no insurance or not enough coverage.

For example, imagine someone hits your rebuilt car but doesn’t have insurance. Without this coverage, you may have to pay for repairs yourself. With it, your insurance company steps in to cover the costs (depending on your policy).

This coverage is often overlooked, especially by budget buyers trying to save money. But it can be very valuable, particularly in areas where uninsured driving is more common.

For rebuilt cars, this type of insurance is usually easier to obtain than collision or comprehensive coverage. It adds an extra layer of protection without significantly increasing the cost.

What Insurance Companies Require Before Covering a Rebuilt Vehicle

Before an insurance company agrees to cover a rebuilt title car, they want proof that the vehicle is safe, properly repaired, and legally approved for the road. This is their way of reducing risk.

For budget buyers, this step often feels like extra work. But without these documents, getting insurance can be difficult or even impossible.

Think of it from the insurer’s perspective: they are not just insuring a car — they are insuring a car with a damage history. So they need clear evidence that everything has been fixed correctly.

Here are the most common things insurers will ask for.

State Salvage Inspection Certificate

This is one of the most important documents. It proves that the car has passed a state inspection and is officially considered roadworthy.

The inspection usually checks:

- safety systems (brakes, airbags, lights)

- structural integrity

- proper installation of parts

Without this certificate, most insurance companies won’t even consider offering a policy. It shows that the car has moved from salvage status to rebuilt status and meets basic safety standards.

For example, if you repaired a car yourself but never completed the inspection process, insurers will treat it as too risky — even if it looks perfect.

Proof of Repairs and Parts Receipts

Insurance companies want to see exactly what was repaired and how. This is why keeping all documentation during the repair process is critical.

You may be asked to provide:

- receipts for parts

- invoices from repair shops

- a list of replaced components

This helps insurers understand the quality of the repairs. It also reduces the risk of fraud, such as using stolen parts or skipping important fixes.

For example, if you replaced major components like airbags or suspension parts, showing receipts proves the work was actually done. Without that proof, the insurer may assume the repairs were incomplete or low quality.

Photos of the Vehicle

Photos are another key requirement. Insurance companies often ask for pictures showing:

- the car before repairs (damage condition)

- the repair process

- the final result after repairs

These images give a visual record of what happened to the car and how it was restored.

For budget buyers who fix cars themselves, this step is easy to overlook. But taking photos along the way can make a big difference later when applying for insurance.

For example, clear “before and after” photos can reassure the insurer that the damage was not as severe as it might sound on paper.

VIN Verification and Vehicle History Report

Finally, insurers usually require VIN verification and a vehicle history report.

The VIN (Vehicle Identification Number) confirms the identity of the car. It ensures that the vehicle matches official records and has not been altered or misrepresented.

A vehicle history report provides details about:

- past accidents

- previous ownership

- title status changes

- mileage records

This helps the insurer get a complete picture of the car’s background.

For example, if the report shows multiple severe incidents or inconsistent mileage, the insurer may decide the risk is too high. On the other hand, a clean and consistent history (aside from the salvage event) can improve your chances of getting better coverage.

In simple terms, the more transparent and well-documented your rebuilt car is, the easier it will be to insure.

Estimate the Full Cost Before You Commit

A lower purchase price is only part of the equation. Before buying a salvage or rebuilt title car, calculate auction fees, transportation, repair-related costs, and export expenses to understand the real total cost of ownership.

- ✅ Transparent service pricing

- ✅ Help estimating total landed cost

- ✅ Vehicle history data for better risk review

- ✅ Support before purchase and shipping

Does It Cost More to Insure a Rebuilt Title Car?

Yes, insuring a rebuilt title car usually costs more than insuring a similar car with a clean title. Insurance companies view rebuilt vehicles as higher risk because of their damage history. The final premium depends on several factors, and understanding them can help budget buyers make smarter choices.

For example, two buyers may purchase the same make and model: one with a clean title and one rebuilt. Even if the cars look identical after repairs, the rebuilt car will almost always have a higher insurance rate.

Factors That Affect Insurance Rates

Several factors influence how much you’ll pay to insure a rebuilt title vehicle. The insurer evaluates both the car and the driver to set the rate.

Vehicle Value After Repairs

The car’s post-repair market value plays a major role. Since rebuilt cars are worth less than clean title cars, insurance payouts are usually lower. Insurers factor this into your premium.

For example, a rebuilt car valued at $8,000 will cost less to cover than a similar car worth $15,000, but the coverage may also be limited. If your car is damaged again, the payout may not cover all repair costs.

Repair Quality and Safety

Insurance companies also look at how well the car was repaired. Poor repairs or use of substandard parts increase the risk of future accidents or failures.

For example, if a car had frame damage and it was poorly repaired, the insurer might see it as a higher risk. A vehicle repaired by a professional shop using quality parts is likely to have lower premiums than one repaired cheaply by a hobbyist.

Driver History and Location

Your personal driving record and where you live also impact insurance costs. Drivers with clean records pay less, while those with accidents or tickets pay more. High-risk areas with frequent theft, flooding, or accidents may increase premiums.

For instance, a rebuilt car in a busy urban area might cost more to insure than the same car in a rural town due to higher accident and theft risk.

Why Some Policies Are Cheaper but Offer Less Coverage

Some insurers offer lower rates for rebuilt cars by limiting the coverage. For example, you may get liability insurance only or reduced collision and comprehensive limits.

This can be tempting for budget buyers, but it comes with trade-offs. If your car is damaged, you may receive a smaller payout, or certain types of damage might not be covered at all.

For example, a cheaper policy might exclude coverage for theft or flood damage. While it saves money monthly, you could end up paying thousands out of pocket if something happens.

In short, insuring a rebuilt car is usually more expensive than a clean title car, but careful research and understanding the coverage options can help you balance cost and protection.

How to Get Insurance for a Salvage or Rebuilt Title Car

Getting insurance for a salvage or rebuilt title car can feel complicated, but breaking it into clear steps makes the process manageable. Budget buyers often worry about cost and coverage, but following a systematic approach can help you secure insurance without unnecessary stress. Here’s a step-by-step guide.

Step 1: Convert the Salvage Title to a Rebuilt Title

Before you can get standard insurance, a salvage title must be converted into a rebuilt title. This involves repairing the car and proving it meets state safety requirements. Until this is done, most insurance companies will refuse coverage for driving on public roads.

For example, if you buy a salvage car at an online auction, it may be cheap upfront, but it’s essentially a “project car” until you convert the title. Completing this step is essential before you can legally insure and drive it.

Step 2: Pass a State Inspection

Once the car is repaired, it must pass a state-mandated inspection. This inspection verifies that the vehicle is safe and roadworthy. Inspectors will check the frame, brakes, lights, airbags, and other critical systems.

Passing this inspection is a legal requirement for a rebuilt title and a necessary step for insurance. For budget buyers who do repairs themselves, scheduling and passing this inspection ensures that insurers recognize the car as safe and eligible for coverage.

Step 3: Gather Repair Documentation

Insurance companies will want proof of all repairs. This includes receipts for parts, invoices from repair shops, and photos showing before-and-after conditions.

Detailed documentation reassures insurers that repairs were done properly and with quality parts. For example, if a car had engine or frame damage, providing receipts and photos shows that the repairs were completed correctly, increasing the chances of getting full coverage.

Step 4: Request Quotes From Multiple Insurers

Once your rebuilt title car is ready, start requesting insurance quotes from several companies. Rates and coverage can vary significantly between providers, so shopping around is crucial.

Budget buyers benefit from comparing both cost and coverage. Some insurers may offer lower rates but limit coverage options, while others may be slightly more expensive but provide full protection. Getting multiple quotes ensures you can make an informed decision.

Step 5: Compare Coverage and Limitations

After receiving quotes, carefully compare what each policy includes and excludes. Check coverage types (liability, collision, comprehensive), deductibles, payout limits, and any restrictions specific to rebuilt title vehicles.

For example, one insurer may exclude flood or fire damage, while another includes it. Another may offer a lower premium but limit collision coverage. Understanding these differences helps you choose a policy that balances affordability with protection, which is especially important for budget-conscious buyers.

Which Insurance Companies May Cover Rebuilt Title Vehicles

Finding an insurer for a rebuilt title car can feel tricky, but many companies do provide coverage if the proper documentation is in place. The key is knowing where to look and understanding the differences between providers. Budget buyers can save both time and money by targeting companies familiar with rebuilt vehicles.

Insurance options generally fall into three categories: large national insurers, regional providers, and specialty companies that handle high-risk vehicles. Each has advantages and limitations.

Large National Insurers

Big insurance companies like State Farm, GEICO, and Progressive often provide coverage for rebuilt title vehicles. They have the resources to handle higher-risk cars and may offer a variety of coverage options, from basic liability to full collision and comprehensive insurance.

However, national insurers may charge higher premiums for rebuilt cars, reflecting the perceived risk. Some may also require extensive documentation, including inspection certificates, receipts, and photos, before providing coverage.

For example, a buyer who purchases a rebuilt vehicle from an online U.S. auction may get a quote from a large national insurer that offers full coverage, but the monthly premium could be 20–40% higher than a clean title car of the same model.

Regional Insurance Providers

Regional insurers are often more flexible with rebuilt title cars. They may have experience with local salvage and rebuilt vehicles and may be willing to work with smaller budgets.

These companies can sometimes offer lower premiums than national insurers while still providing adequate coverage. They may also be more understanding of repair documentation from local shops.

For example, a rebuilt car in Texas might be easier to insure with a regional company familiar with local state inspections and salvage laws. Budget buyers often benefit from contacting regional insurers directly, especially if national companies offer limited options.

Specialty Insurers for High-Risk Vehicles

Specialty insurers focus on high-risk or unusual vehicles, including rebuilt title cars, classic cars, and modified vehicles. They understand the unique challenges of insuring cars with a history of significant damage.

These companies often offer policies that are not available through mainstream insurers. For instance, they may provide full coverage for rebuilt cars with comprehensive documentation or offer project car policies while repairs are ongoing.

For budget buyers, specialty insurers can be a lifesaver when traditional companies refuse coverage. While premiums may still be higher than for clean title cars, specialty insurers provide the flexibility and protection that standard policies might not.

Why Insurance Companies Are Careful With Salvage Vehicles

Insurance companies approach salvage vehicles with extra caution because these cars carry a history of serious damage. Even after repairs, insurers see them as higher-risk compared to clean title vehicles. Understanding the reasons behind this caution can help budget buyers anticipate challenges when seeking coverage.

Insurers assess risk to determine premiums, coverage options, and payout limits. Salvage vehicles create uncertainties that make standard policies more complicated or expensive.

Here are the main factors that make insurance companies cautious.

Higher Risk of Hidden Damage

Salvage vehicles often have hidden damage that may not be obvious even after repairs. Structural issues, weakened frames, compromised safety systems, or electrical problems can remain undetected during repairs.

For example, a car that has been in a major collision may look perfectly repaired, but the alignment or frame integrity could still be compromised. These hidden issues increase the likelihood of future accidents or mechanical failures, which makes insurers hesitant to provide full coverage.

Budget buyers sometimes underestimate this risk, assuming that cosmetic repairs are enough. Insurance companies know that hidden damage can lead to expensive claims, so they either charge higher premiums or limit coverage.

Difficulty Determining Actual Car Value

Another challenge is determining the true market value of a salvage vehicle. After significant damage, there’s no standard resale value like there is for clean title cars.

For example, two cars of the same make, model, and year could have drastically different rebuilt quality. One might have professional repairs and high-quality parts, while another could have minimal fixes. Insurers find it difficult to set premiums and predict potential payouts without clear valuation.

This uncertainty means insurers may offer lower payout limits or increase premiums to protect themselves. Even if a car looks flawless, its past history affects how much the insurer is willing to pay in case of a claim.

Increased Risk of Fraud

Fraud is another concern for insurance companies when dealing with salvage vehicles. Unscrupulous sellers might misrepresent the car’s damage history or use stolen parts in repairs. There’s also the risk of inflated repair invoices or falsified documentation submitted to get insurance approval.

For example, a buyer might unknowingly purchase a car with unreported flood damage or a rolled-back odometer. Insurance companies are cautious because these situations can lead to fraudulent claims or disputes over payout amounts.

To reduce risk, insurers require detailed documentation, state inspection certificates, and vehicle history reports before offering coverage. These measures protect both the insurer and the buyer from hidden problems.

Pros and Cons of Insuring a Salvage or Rebuilt Title Car

Insuring a salvage or rebuilt title car comes with both benefits and drawbacks. For budget buyers, understanding these pros and cons is essential before committing to a purchase. While these cars can offer significant savings upfront, the insurance process and coverage limitations require careful consideration.

Knowing what to expect helps you make a smart decision and avoid surprises if you need to file a claim in the future.

Advantages for Budget Buyers

The biggest advantage of a salvage or rebuilt title car is the lower purchase price. These vehicles are often sold for 20–50% less than similar cars with clean titles. For someone on a tight budget, this can make a big difference — you can get a newer model or a car with better features for the same money.

Additionally, insurance for rebuilt title cars, while sometimes more expensive than for clean title vehicles, can still be manageable. If you focus on minimum required coverage, like liability insurance, you can legally drive the car at a relatively low cost.

For example, a buyer may find a 2015 sedan with a rebuilt title for $8,000 versus $14,000 for a clean title version. Even with slightly higher insurance premiums, the overall savings are substantial.

Potential Risks and Limitations

The main drawback is the increased risk and limitations associated with coverage. Insurance companies may restrict certain types of insurance or impose lower payout limits. Collision and comprehensive coverage may be limited, or some companies may refuse full coverage altogether.

Another risk is hidden damage. Even if the car passes inspection, unseen structural or mechanical problems could arise later. This could lead to higher maintenance costs or difficulty getting repairs covered by insurance.

For example, a rebuilt car that had frame damage in a previous accident might develop alignment issues years later. Some insurers might deny claims for pre-existing problems, leaving the owner responsible for repairs.

Lower Payouts in Case of Future Claims

Another important consideration is that insurance payouts are generally lower for rebuilt title cars. Since these vehicles are worth less than comparable clean title cars, the insurance company calculates claims based on their reduced market value.

For instance, if a rebuilt car is damaged in another accident, the payout may only cover $6,000 for a car that would have fetched $12,000 with a clean title. This is a trade-off buyers make in exchange for saving money on the initial purchase.

Tips for Buying a Salvage Car If You Plan to Insure It

Buying a salvage car can be a smart way to save money, but if you plan to insure it, careful planning is essential. Not every salvage vehicle is a good candidate for rebuilding, and not every car will qualify for affordable insurance after repairs. Following a few practical tips can help you avoid costly mistakes and ensure your investment is safe and insurable.

For budget buyers, these steps can make the difference between a bargain and a headache.

Choose Vehicles With Repairable Damage

The first rule is to select cars with damage that is relatively easy and safe to repair. Cosmetic damage like dents, scratches, or minor bumper damage is usually manageable. Moderate mechanical or engine repairs can also be acceptable if you have access to a qualified mechanic.

Avoid vehicles with complicated structural issues or multiple system failures unless you have experience or professional support. For example, a car with a damaged fender and broken headlights can usually be fixed quickly and inexpensively. A car with severe engine, transmission, or frame damage may end up costing far more than its market value once repaired.

Avoid Severe Frame or Flood Damage

Certain types of damage make insuring a rebuilt car very difficult. Severe frame damage can compromise safety even after repairs, and flood damage can create hidden problems like corrosion and electrical failures.

For example, a car submerged in floodwater might look fine on the surface, but wiring, sensors, and the engine may fail months later. Insurers often charge higher premiums or refuse coverage altogether for such vehicles. Budget buyers should prioritize cars with clean structural integrity and avoid water-damaged vehicles, even if the price is tempting.

Check Insurance Availability Before Buying

Before placing a bid or completing a purchase, always verify that insurance will be available. Contact multiple insurance companies or agents to ask about coverage options for the specific car you’re considering.

Ask about requirements such as rebuilt title status, inspection certificates, repair documentation, and coverage limitations. For instance, a car may be inexpensive at auction, but if no insurer will offer full coverage after repairs, it could become a costly and risky purchase.

Is It Worth Insuring a Salvage Title Car?

Deciding whether to insure a salvage title car depends on your goals, budget, and the condition of the vehicle. For some buyers, it can be a smart way to save money, but for others, it may create more hassle than it’s worth. Understanding the factors that influence this decision can help you make a practical choice.

Budget buyers should weigh the upfront savings against future costs, insurance limitations, and potential repair issues.

When It Makes Financial Sense

Insuring a salvage or rebuilt title car makes financial sense when the purchase price is low and the repairs are straightforward. If you can buy a car significantly below market value and repair it at a reasonable cost, you can end up with a functional vehicle for far less than a clean title car.

For example, a 2016 sedan with minor collision damage might sell for $6,500 with a salvage title, compared to $12,000 for the same car with a clean title. After $2,000 in repairs and inspection, you could legally insure and drive the car, still saving thousands compared to buying a similar clean title vehicle.

It also makes sense if you only need basic coverage. Liability insurance may be enough to meet legal requirements and keep monthly costs low. For budget-conscious buyers who prioritize low purchase and insurance costs over maximum resale value, this can be a smart strategy.

When It May Be Better to Avoid Salvage Vehicles

On the other hand, it may be better to avoid salvage vehicles when damage is extensive or complicated, or when insurance options are very limited. Cars with severe frame damage, flood history, or multiple major repairs often come with higher insurance premiums, lower coverage, and ongoing maintenance issues.

For example, a car with prior flood damage may look clean but could have hidden electrical or engine problems. Even if you can insure it, future claims might be denied for pre-existing issues, leaving you responsible for costly repairs.

If your goal is long-term reliability, resale value, or comprehensive insurance coverage, a salvage car may not be worth the risk. Sometimes paying more upfront for a clean title car provides better overall security and fewer surprises down the road.

Final Thoughts: Insurance and Salvage Title Cars

Insuring a salvage or rebuilt title car is a unique challenge, but it’s not impossible. For budget buyers, these vehicles offer a way to own a car at a fraction of the cost of a clean title vehicle, yet they come with important trade-offs. Understanding the process, the risks, and the limitations of insurance is key to making a smart decision.

The journey typically begins with purchasing the salvage car, completing necessary repairs, passing state inspections, and obtaining a rebuilt title. Only then can you apply for insurance and legally drive the vehicle. Skipping any of these steps can lead to problems, including denial of coverage or legal issues on the road.

Insurance premiums for rebuilt title cars are generally higher, and coverage may be limited. Hidden damage, uncertain market value, and insurer caution all contribute to these challenges. Budget buyers need to weigh these costs against the initial savings on the purchase price.

However, with proper preparation, documentation, and careful selection of vehicles, salvage and rebuilt title cars can be a practical and affordable option. Choosing cars with repairable damage, verifying insurance availability before buying, and maintaining thorough repair records all increase the likelihood of obtaining coverage.

Browse Salvage and Rebuilt Cars With More Confidence

If you now understand how title status affects insurance, cost, and long-term value, you can move from research to action. Explore available auction inventory, compare vehicle history, and make a more informed buying decision before placing your bid.

- ✅ Free membership registration

- ✅ Unlimited bidding through a licensed broker

- ✅ Auction history reports on available vehicles

- ✅ Support from purchase to delivery

Further Reading

Salvage Title Meaning: What You Need to Know

Understanding Salvage vs. Clean Titles: What Buyers Need to Know

Salvage Car Facts Debunked! Top 4 Misconceptions About Salvage Title Car

Buy Salvage Cars from the USA. What's the Meaning and Benefit?